At some point in the mortgage application process, you'll get asked questions about your race, ethnicity, gender, and age. Being asked to provide this information can often raise a question of your own: Why?

Let's answer that question now.

Clearing up anti-discrimination laws

A law called the Equal Credit Opportunity Act (ECOA) enacted in 1974 makes it illegal for lenders to discriminate based on race, national origin, gender, age, marital status, or because one receives public assistance.

Another law called the Home Mortgage Disclosure Act (HMDA) enacted in 1975 requires lenders to collect, report, and disclose a long list of data about mortgages they originate, including each borrower's race, ethnicity, gender, and age. This HMDA data helps regulators determine if lenders are serving the housing needs of their communities, identify possible discriminatory lending patterns, and assist public officials in making community housing investment decisions.

So ECOA says lenders can’t use race, ethnicity, gender, and age to make loan decisions. And HMDA says lenders must ask for race, ethnicity, gender, and age to monitor for discriminatory patterns.

How are these questions asked in the loan process?

A form called the Universal Residential Mortgage Application contains all of the borrower questions required by federal law.

Your age is obtained by requesting your date of birth.

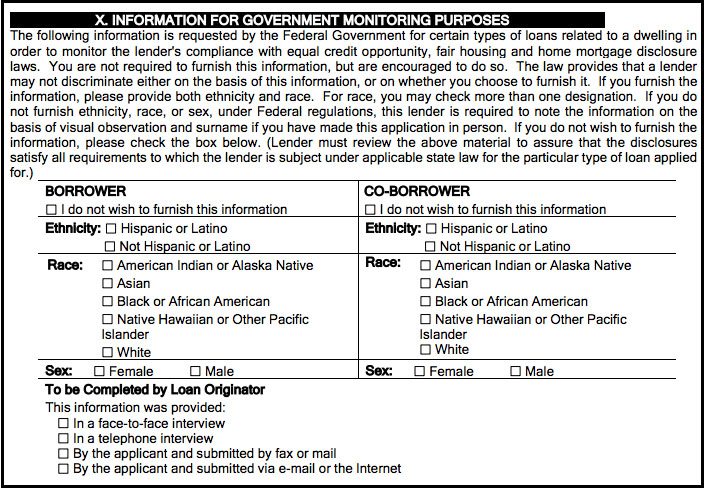

Race, ethnicity, and gender are requested in a specific categorical format required by federal law as shown in the image below.

The fine print of this section in a loan application contains three concepts that are especially important:

- You are not required to provide this information, but are encouraged by the government to do so.

- The law provides that a lender may not discriminate either on the basis of this information, or on whether you choose to furnish it.

- If you've made the application in person and do not furnish ethnicity, race, or gender, federal law requires your lender to note the information on the basis of visual observation and last name.

You should also note that as technology streamlines your application process, these questions may not be asked or visually presented in this format - but they will be asked.

Changes to these questions coming soon

HMDA rules are enforced by the Consumer Financial Protection Bureau (CFPB), and the CFPB has already made new laws to improve HMDA data collection. The new laws go into effect on January 1, 2018.

It's worth knowing about these changes now because lenders will be working toward these changes between now and January 2018.

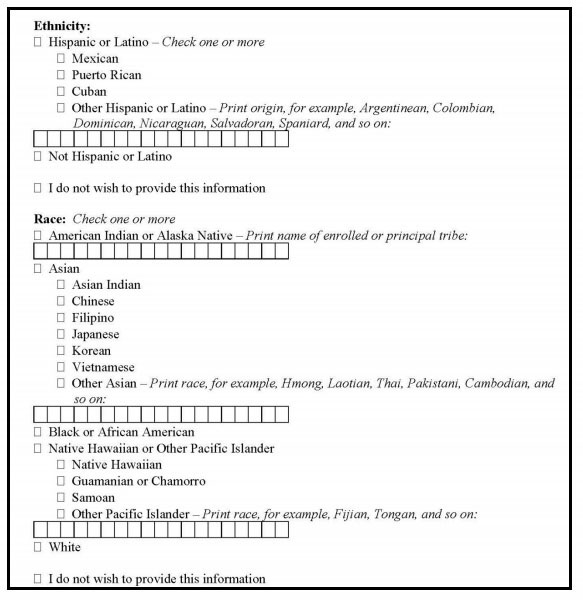

Revised HMDA laws fine-tune requirements for lenders when collecting race, ethnicity or gender from borrowers who choose to furnish this information versus those who choose not to furnish it.

If a borrower chooses to provide race and ethnicity under the revised laws, they will get an expanded set of categories to select from, as shown here.

However, if a borrower chooses not to provide race and ethnicity when applying in person, the lender must use the same categories while following the same visual observation and last name requirements they follow today.

The CFPB ruled that allowing borrowers to self-identify using newly expanded categories and requiring lenders to identify (when borrowers choose not to) using today's limited categories is the best balance of consumer protection and lender regulatory burden.

What to do if you feel discrimination has occurred

As you can see, our federal regulators think deeply about consumer protection, but no law is perfect at interpreting your individual loan experience.

If you are concerned about mortgage discrimination or believe you have been discriminated against, follow the CFPB’s complaint process, or call the CFPB at 855-411-2372.

Related:

- 5 Mortgage Misconceptions Set Straight

- Can the Mortgage Process Really Be 100% Digital?

- The 4 Most Important Mortgage Documents You’ll Sign

from Zillow Porchlight | Real Estate News, Advice and Inspiration http://www.zillow.com/blog/race-question-on-loan-application-196006/

via Reveeo

No comments:

Post a Comment