Selling this mansion in suburban Chicago ought to be a slam dunk for retired basketball star Scottie Pippen, who’s asking $3.1 million.

The 10,000-square-foot spread gives new meaning to the term “home court advantage” with a basketball court painted with a larger-than-life version of Pippen’s No. 33 jersey from the Chicago Bulls.

A short drive from Lake Michigan, this estate gets in the lane with 2.9 acres that include an infinity pool, spa and slide. There’s lots of room for plays with a two-story living room, a recreation room, sauna and steam rooms, and a wine cellar.

It runs the floor with 5 bedrooms and 5.5 baths, including two master suites and a soaking tub big enough to relax even an Olympic “Dream Team” player. But if you’re looking for something even bigger, Michael Jordan is still trying to sell his estate just down the street.

Financial market turmoil can be good for mortgage rates. Don't forget this concept as you continue to read headlines about how a "Brexit" is wreaking havoc on markets.

Brexit is slang for Britain's vote Thursday, June 23 to exit the European Union (EU), which is a political and economic union allowing free trade and movement of people among 28 member countries.

This outcome was unexpected, and caused stock markets around the world to nosedive.

Mortgage rates approach record lows

The Brexit vote also caused U.S. mortgage rates to nosedive. Rates were down .125 percent the day after the Brexit vote, and are now approaching all-time record lows as 30-year fixed rates move below 3.5 percent.

Why? Because Brexit uncertainty is causing investors to sell riskier global stocks and buy safer U.S. mortgage bonds - which are among the safest bonds in the world because they're comprised of U.S. home loans approved using the strictest guidelines in decades.

When bond prices rise on this buying, bond yields (or rates) drop. When rates drop, it’s often a good time to refinance your mortgage.

To put it in perspective: On a $300,000 loan, if you refinanced at a rate dip of .25 percent, your payment could be lowered by $42 per month.

Mortgage rate outlook from here

When markets are driven more by politics than economics, rate movement will be especially unpredictable. If this Brexit-driven rate dip meets your financial objectives, you should work with your lender to refinance at this lower rate.

Some projections call for rates to rise gradually as Brexit concerns wane, but, conversely, there is also a growing consensus that ultra-low rates may be here to stay.

If you have the stomach to watch rate markets a bit longer, Brexit isn't the only factor driving lower rates. Forthcoming Brexit negotiations may inspire other EU countries to seek independence, which would fuel market turmoil and keep U.S. rates low.

This sentiment has already caused the Federal Reserve to pause its rate hike campaign, citing non-U.S. factors as contributing to increased risk of U.S. recession.

These conflicting predictions mean rate movement will be especially unpredictable in the coming months, so it's best to lock rate dips that meet your financial objectives. Your lender can help you with your objectives and mortgage math.

Tips for refinancers

Thinking of refinancing to take advantage of the low rates? Here are a few tips.

Ensure your lender is quoting correctly. Rate quotes are predicated on a loan closing in a certain number of days. Longer rate locks have higher rates, and lock extensions can eat away refinance savings. If you see one rate quote lower than another when you shop, ask that lender what their rate lock period is, and make sure they can close your loan within their rate lock period.

Ask about timing. Lenders get extremely busy during rate dips, so ask your lender to confirm that they're quoting a rate that allows them enough time to close your loan. (If they can’t, you can look into finding a new lender.)

Don't forget your second mortgage. Your second mortgage holder must agree to the terms of your new first mortgage refinance before the refinance can close. This is required even if you have a Home Equity Line of Credit (HELOC) with a zero balance. This step will add time to the process, so make sure lenders you're shopping with know this as they're quoting rates.

Get ready to provide documents again. Even if you refinance with a lender you've worked with before, federal laws require them to update your employment, income, asset, and debt documentation for a new loan.

When do refi costs break even? A typical refinance costs $2,000 to $4,000, depending on your market. Interest cost savings from the refi should repay closing costs within 24 to 36 months. A refinance calculator can help you estimate your breakeven time.

And don't forget that a "no-cost" refinance isn't actually without cost. You're just accepting a higher rate to enable your lender to credit closing costs. Make sure your lender compares long-term savings of cost vs. no-cost refi options.

Reminder for home buyers

A rate lock runs with a borrower and a property, so as a home buyer, you cannot lock a mortgage rate until you're in contract to buy a home.

Rate dips like the current one tipped off by the Brexit vote benefit you as a home shopper because you'll likely get to lock a lower rate when you get into contract. But until then, you're subject to daily rate market movements.

Kelley Libby lives in an apartment with a view of the Richmond, VA skyline from her balcony. She rides her bike downtown regularly for dinner and a show, or sometimes to take a cool dip in the river.

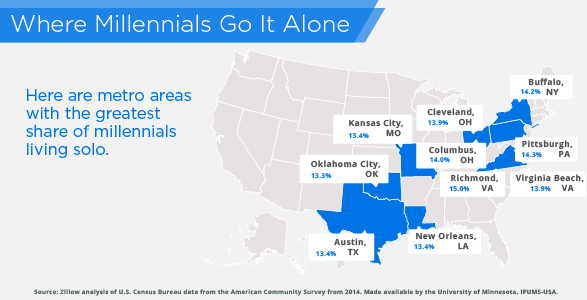

A top-of-the-millennial-pile 34 years old, she is among the 15 percent of millennials who live alone in Richmond, the metro area where a greater share of millennials live solo than anywhere else in the country. Others in the top 10 are Pittsburgh; Buffalo; Columbus, OH; Virginia Beach; Cleveland; New Orleans; Austin; Kansas City and Oklahoma City.

"With home prices and rents rising as fast as they are, it's a common assumption that young adults in many cases cannot afford to live alone," said Zillow Chief Economist Svenja Gudell. "Though that may be true in some markets, there's still a large number of amazing places across the U.S. that are prime for millennials to thrive independently. These are places where young adults can easily find jobs at a competitive salary, and where housing expenses won't eat up the majority of their income, enabling them to save more."

Low rents help

Rents are relatively easy on the budget in many of the metros where millennials live alone. In Richmond, people of all ages typically spend 26 percent of their incomes on rent, compared to 30 percent nationally, according to Zillow Research. In a place where millennials living solo make a healthy $49,500 a year (median) and employment is up 3.6 percent since a year ago, that makes for an attractive package.

“It’s a good place for young, single people, because there’s lots to do as far as cultural activities and outdoor stuff,” said Libby, who’s a public media producer working on a national project called Finding America. She pays $960 a month for her 1-bedroom, which is in a new apartment complex and has that sweet balcony.

It’s also a great place to settle down, and many of her friends are snapping up real estate. “I have so much more of a chance to buy a place here than I would in big, popular cities,” she said.

She lived for several years in nearby Charlottesville, where “I couldn’t dream of buying a house.” The median home value there is $232,700, well above Richmond’s $193,200, according to Zillow data.

Often they do it in places where rents are more affordable — areas like Pittsburgh, Kansas City and Oklahoma City, where rents take up around 25 percent of people's incomes. They also go solo in metros like Virginia Beach where they can afford to buy homes, and places like Austin with strong employment growth.

Malory Berschet has lived on her own in Columbus for a year, following stints with her parents and with a college roommate. She enjoys it, but she’s had to cut back to make her $1,125 monthly rent.

“My biggest thing was spending money like I was made of money,” said Berschet, who’s 25. “I would eat out all the time or buy lunch rather than pack it. And I don’t need 100 channels on cable.”

Millennials living alone make $38,800 a year (median) in Columbus, where people spend 26 percent of their incomes on rent.

Berschet knows coworkers at Cardinal Health, where she’s a market manager, who save money by living in Dublin, the suburb where the company is headquartered. They pay less in rent and have better commutes, Berschet said, but “they’re a good 20 minutes from downtown.” She likes being close in, where she can easily walk or Uber to visit friends and eat out.

Less solo-friendly cities

At the other end of the spectrum, she has a friend who’s moving to San Francisco and said the rent is $3,500 for an apartment smaller than Berschet’s 1-bedroom — which makes her place seem like a steal.

Only 9.4 percent of millennials live alone in the San Francisco area. It’s not the smallest share of independent millennials in the country — that’s Riverside, CA, with 6.1 percent. They make good money — $66,000 for millennials living alone in San Francisco and $72,000 in Riverside (medians) — but people who live in those places spend 46 percent and 36 percent of their incomes, respectively, on rent.

Prices like that can make roommates — and even Mom’s basement — look mighty appealing.

While a large number of millennials are finding themselves back at home with Mom and Dad, many young people prefer to set out and make it on their own.

Not everyone wants a roommate, and securing a place that is all yours signifies true adulthood for many people.

This impressive 1-bedroom loft brings vintage charm with its exposed wood beam ceilings and exposed brick walls. The elegant wood floors, along with the stylish kitchen, ensure that this loft is a dream first apartment. In Richmond, 15 percent of millennials live alone, and their median income is $49,500.

With a great living area featuring plush carpet, this spacious 1-bedroom boasts picture windows throughout, as well as enough room for separate dinning. The kitchen includes a breakfast bar, granite countertops, stainless steel appliances and warm wood cabinets. Millennials living in Pittsburgh have a median income of $40,000 and 14.3 percent of people are going it alone.

You’ll love coming home to wood flooring, high ceilings with exposed beams and concrete walls with brick accents. Large windows offer city views, as well as a glimpse of Niagara Falls, and the large living area connects to the open kitchen with an island. This 1-bedroom also comes equipped with a large walk-in closet with built-in shelving, along with an extraordinary all-glass shower. Buffalo Millennials earn a median income of $40,000, and 14.2 percent of them live on their own.

This charming 1-bedroom provides an inviting atmosphere with plush carpet, in-home washer and dryer, and large closets and picture windows. The kitchen includes dark cabinets and attractive plank flooring, along with all-black appliances. Fourteen percent of Columbus millennials live by themselves, and the median income is $38,800.

Find high-rise living at its best in this 1-bedroom apartment. With a beach-friendly color scheme and ample space for entertaining and dining, comfort abounds. Large windows introduce wonderful views and natural light, while the separate kitchen features bright paint and a buffet window. The median income for millennials in Virginia Beach is $50,000, and 13.9 percent live by themselves.

Multi-colored walls, wide open spaces and lake views await in this 1-bedroom apartment, which once served as a hotel. This vibrant home ensures comfort at every turn with carpet throughout, a bathroom offering vanity lights, and a large kitchen with counter space for dining. In Cleveland, 13.9 percent of millennials live alone, and their median income is $35,000.

Soaring above the city, this 1-bedroom offers a classic feel with simple elegance and light-colored plank flooring. Crisp white walls provide an airy feeling throughout the space, which includes a galley kitchen, large windows and track lighting. New Orleans millennials earn a median income of $40,000, and 13.4 percent of them live solo.

It will be hard to pull yourself away from the private balcony connected to this modern 1-bedroom dwelling. Accent walls, plank flooring and a separate space for an in-home washer and dryer, complement the large open kitchen and dining room. Additional perks include a spacious bathroom and a walk-in closet. In Austin, 13.4 percent of millennials live alone, and they have a $40,000 median income.

A private entryway leads into this 1-bedroom apartment complete with a balcony. Plush carpet will make you feel comfortable inside the spacious home, while large windows ensure natural light. The home boasts a kitchen large enough to include a pantry, as well as the entrance to the washer and dryer closet. Kansas City millennials have a median income of $40,000, and 13.4 percent of them live alone.

Picture windows, granite countertops and plank flooring await inside this 1-bedroom. Enjoy the convenience of a private balcony, stainless steel appliances, a kitchen island, and an in-home washer and dryer. In Oklahoma City, the medium income is $40,000 for millennials, and 13.3 percent of them live alone.

On their own, tiny homes pack a hefty punch. They’re environmentally friendly, efficient, affordable and pretty darn cozy.

But, when paired with long summer days and the great outdoors awaiting your enjoyment, living small is a no-brainer.

Perfect for spending hot days in the water and balmy nights snuggled by the campfire, the 10 following micro homes are perched on oceans, lakes, and rivers across the United States. And considering the adorable interior designs and scenic views, a rainy day or two wouldn’t be the worst thing.

Surrounded by beach roses and the cobalt Atlantic waters of Mattapoisset Harbor, this 538-square-foot beach cottage is the perfect New England summer getaway. Despite being petite, this 2-bedroom, 1-bathroom home is ready for extra guests; one bedroom is equipped with bunk beds, and the open concept living/dining area is impressively spacious.

Nestled on Silver Lake, this 576-square-foot cottage offers 100 feet of lake frontage, complete with a wraparound deck to enjoy some stellar sunsets - and perhaps even a greeting from the nearby resident eagle. Activities like water skiing and canoeing are just steps away, while the newly renovated interior of this 2-bedroom, 1-bathroom home features hardwood floors and pleasant pastel tones.

Encompassed by towering trees, this private, 600-square-foot cottage is perched on Cottonwood Bay on the beautiful Coeur d’Alene Lake. One hundred feet of lake frontage put countless lake activities at your fingertips, while the 1-bedroom, 1-bathroom home is fully furnished and endowed with spectacular views.

Located in Raspberry Cove and just minutes from downtown Freeport, this 581-square-foot oceanfront cottage is ready for your canoes, kayaks, and summer cookouts. The gorgeous, sun-drenched interior of this 1-bedroom, 1-bathroom home features huge windows, an updated kitchen and bath, and a sleeping porch.

This 3.32-acre riverfront property is the ideal setting for a NorCal summer getaway, complete with a 679-square-foot home, wraparound deck, Jacuzzi, and picnic area overlooking the Russian River. The interior walls of this 2-bedroom, 1-bathroom home were painted by artist Jorge Nadal, and this location is minutes away from the Pacific Coast, hiking trails, cycling routes, and kayaking.

Located between a 50-foot sandy beach on the Puget Sound and a 50-foot lagoon with a boat launch, this 632-square-foot home in fact has two waterfronts. The Olympic Mountains provide a picturesque background, and seafood fans will love the easy accessibility of clamming and crabbing, as well as a beautiful kitchen to prepare your bounty.

Surrounded by foliage on beautiful Lake Murray, this whimsical, 700-square-foot home is awaiting a new family to make memories with. The completely updated interior of this 1-bedroom, 1-bathroom home has quirky pops of color and a loft with two separate sleeping areas, while the exterior features a spacious deck and waterfront dock.

Perched atop the Kentucky River, this 570-square-foot home offers access to an array of outdoor activities, including fishing, kayaking, canoeing, or simply viewing the nearby waterfall. This 1-bedroom, 1-bathroom home features an additional loft and comes fully furnished with its timeless decor.

Located on a 1.4-acre, waterfront lot on Little Bitterroot Lake, this 690-square-foot rustic cabin comes equipped with a dock, a wraparound deck, and a stone campfire pit. Inside this 1-bedroom, 1-bathroom home, one will find wood-beamed ceilings, an antique wood stove, and a finished basement.

Built to be enjoyed year-round, this 480-square-foot waterfront cabin is located on tranquil Fawn Lake, with access to superior fishing and bird-watching thanks to nearby bald eagle and loon nests. This 2-bedroom, 1-bathroom home has an updated contemporary interior, boasting stainless steel appliances, hardwood floors, wood accents, and pops of red and charcoal.

The agent/seller relationship is like none other. No other professional spends the majority of their client time in the client's actual home. We get very close to our sellers, not just physically but mentally and emotionally.

Because we see them in this somewhat vulnerable setting, and for an extended period, sometimes special bonds form. The line between the business and the personal sometimes blurs, and the seller feels comfortable enough to indulge in some behaviors that drive the agent crazy.

Here are five things sellers do that make agents go nuts - and diminish their chances for a successful sale at the best price and in the shortest amount of time.

Failing to keep the home clean

When your home is on the market, it needs to be ready for a showing on a moment's notice. That means you need be “seller aware” 24/7.

If you're serious about selling, keeping things tidy is par for the course. Make a plan to remove Fido's saliva-stained tennis ball from the couch or Susie's Barbie doll off the floor.

Before you list, move out the stuff you won't need until you settle into your new home. Make a particular space in a closet or storage bin for the day-to-day stuff that could turn off potential buyers. Doing so will only ensure a positive experience for your prospective customer, the buyer.

Sticking around during an open house

There's a reason real estate agents don't want sellers hanging around when potential buyers arrive. While you may be perfectly friendly and agreeable, your presence can alienate your customers or make them feel uncomfortable without you even knowing it.

They want to dig their feet into their potential new home. That means they need to feel free to open closets, poke around in cabinets and make comments to their partners or kids.

Your presence prevents them from getting to know your home - and it can backfire. If you're desperate to find out what’s going on at an open house or how buyers are responding, make a plan with your agent to show up anonymously during the open house.

Holding out for extra money at the last minute

A home sale negotiation can be a rocky road, even in healthy markets. If you sense the market is in your favor, you may second-guess the list price if you see activity quickly, particularly in the form of multiple offers.

It's a great and powerful feeling. But imagine if, in an attempt to squeak out an additional $3,500 from a serious buyer, you pit them against a not-so-great buyer, and you lose both?

It happens, much to the dismay of the listing agents who advocate working with the best buyer and not necessarily the best "offer."

In other words, you should always be thinking of the big picture - which isn't always the same as the most significant offer.

Neglecting to clean up for the new buyer

Imagine you’re the buyer. Would you want to walk into your new home and find 12 cans of old paint in the garage? How about an old baby carriage in the attic?

Clean your home and deliver it in good condition to the new buyers. Not only will they appreciate the gesture, but they’re more likely to be on your side if you need them in the future for favors like forwarding mail or packages.

Insisting your home is unique

Your home is no doubt very special to you. You've built memories, tracked major life events and used it as more than just a place to lay your head at night. When it comes time to sell, it's often hard to think of your home as a product on the open market.

Because of your emotional attachments to it, you may feel your place is unique, which you then equate to being more valuable.

If you find yourself resisting your agent's pricing advice, take a step back and consider if you're ready to sell. Resisting may be a sign you're not yet willing to emotionally detach.

Keep in mind that an overpriced home, even in a strong market, will ultimately sell for less than a home priced well from the start.

The home where Samantha Baker faced her sixteenth birthday with adolescent aplomb is on the market — a 3,250-square-foot colonial home in suburban Chicago.

For $1.499 million, you can have 6 bedrooms, 6 baths and all the “Sixteen Candles” nostalgia you can handle, including the front window where Molly Ringwald sat beside a lit-up birthday cake and kissed her crush.

Situated in the tree-lined suburb of Evanston, the home was built in 1931 and has been expanded by the current owners.

Listing agent Jill Blabolil of @Properties said she’s shown the home to serious potential buyers and to looky-loos. “People walk in the front door and say, ‘This is my favorite movie. I have to be able to say I was in the house,'” she said.

Even brokers have brought their children to brokers’ open houses to check out the home that helped kick off a spate of beloved teen movies from John Hughes.

Now the home has even more space for ’80s-movie loving fans. In addition to renovating the kitchen and bathrooms, the current owners finished the third floor, adding a family room plus a bedroom and bathroom. For taking the party outside, they also installed a backyard kitchen, wood-burning fireplace, stone terrace and television.

In case you’d like a set of homes to celebrate your love for the classic film, Molly Ringwald’s historic co-op in Manhattan’s East Village is also on the market. Asking price: $1.795 million.

Home shoppers eager to qualify for a mortgage could get turned down because of a number they've never heard of: their debt-to-income ratio (DTI).

If you're a bit hazy on DTI, you're in good company. According to Fannie Mae's Economic & Strategic Research (ESR) Group, more than half of consumers surveyed weren't sure what it is either.

And, in this case, what they don't know could hurt them - financially, that is.

High DTI (not credit scores or how much borrowers had in the bank) was the top reason to reject a loan applicant, according to a 2014 FICO study of credit-risk managers covered by The Washington Post.

Understanding DTI

Put simply, DTI is a calculation of your monthly debt payments divided by your gross monthly income.

Lenders calculate DTI in two ways, and both are important. First, they'll add together all your expected housing expenses (your new mortgage, including taxes and insurance) and divide that by your gross (pre-tax) income. That's called your front-end DTI.

Second, they do the same calculation but include all of your monthly expenses, like minimum payments on credit cards and auto loans. That's called your back-end DTI.

For conventional mortgage loans (loans not insured by the government), mortgage lenders are generally looking for 28 percent or lower for the front-end DTI, and 36 percent or lower for the back-end.

"Some lenders may be a little stricter, and others less so," says Cara Pierce, who's worked as a housing financial specialist with Atlanta-based ClearPoint Credit Counseling for 19 years.

Why DTI matters

Your DTI ratio is important, Pierce says, because it's what lenders use to determine how much money they will loan you.

If you’re already using 10 percent or more of your gross income to pay your monthly living expenses, such as car payments and credit card minimum payments, you'd have less than 26 percent for your other housing expenses to stay under 36-percent DTI on the back end.

A DTI higher than 36 percent doesn't mean you won't qualify. In fact, Fannie Mae purchases loans from lenders with back-end DTI ratios as high as 45 percent. But you may want to re-evaluate how much you want to spend on a home - or if it’s even the right time to buy.

Can I lower my DTI?

Lowering your DTI could help you get a lower interest rate "because less debt is generally viewed as a good thing," notes Investopedia.

So if you still want that more expensive home, there are two ways to lower your DTI.

First, pay down debt. Even paying a little over the minimum payment each month on accounts will help. "If you have a $100 a month payment and can't afford $200, just pay $125,” advises Pierce. “That will make it faster for you to pay off the debt.”

Alternatively, you could look for ways for you or your household to raise your income or consolidate your debt.

Either way, it's important to know how lenders calculate DTI, and how a high DTI ratio could affect your chances of being approved for a loan. "People don't understand DTI because it's a math equation," says Pierce, "but it's a number that lenders will use to approve or deny loan applications."

The Baby Boomer generation is proving once again that they’re anything but predictable.

In fact, Boomers are one of the fastest growing groups of renters in the country, and their numbers are expected to grow upwards of 12 million by 2030. While many Boomers are moving into rentals to downsize, others want the flexibility to move to stay close to children and grandchildren.

Whatever the reason for leaving homeownership behind, Boomers have unique needs as renters. Whether you are looking to rent or helping a senior family member find a new home, here are five considerations that you should take into account when looking at a rental.

Low maintenance

One of the greatest benefits of renting is that you are not responsible for maintenance and repairs. When you are looking to rent an apartment or home, make sure that all maintenance is included in the rent, especially if there is a garden or yard that requires upkeep.

If you plan to make the rental a long-term home, it's important to think about how the home will “age” with you in terms of accessibility. Are there a lot of stairs or an elevator? Are cabinets and other storage spaces easily reachable? Is there a shower that can be easily stepped into?

Style and high-end finishes

When making the switch from homeownership to renting, it's important to feel comfortable in your surroundings. Apartments or houses that feature quality finishes on cabinets, countertops, and fixtures can make the transition from homeowner to renter easier. Just because you are renting doesn’t mean you need to sacrifice quality or comfort.

Accessibility

Just like renters in their twenties, Boomers are often looking for places that have access to art, restaurants, and local events. Look for a home that is near the action so you don't have to go too far to join in on the fun.

Updated appliances

Low maintenance is the name of the game when it comes to Baby Boomer-friendly rentals. When looking at a place, make sure the appliances are updated and efficient so you’re not having to deal with constant breakdowns and scheduling repairs. The less you have to be on the phone with the landlord, the more you can enjoy the flexible lifestyle of a renter.

Community events

If you’re looking at an apartment community or complex, be sure to check out what events or socials they offer. Many property managers are responding to the growing number of Boomers in their rental communities and planning events for tenants of all ages.

If you've lived in a home for several decades, you might feel as though you’re leaving a community behind, but there’s no reason you can't build a new one. Barbecues, pool parties, and socials aren't just for millennials - at least not anymore!

Growing up in a tight one-bedroom apartment in the heart of Manhattan, the suburbs seemed downright exotic to me. Everything about them felt foreign, from the sizable houses to the reliance on cars.

By the time I was in middle school I’d already mastered the art of independent NYC public transportation. The parks were my backyard, and having your own room seemed like the epitome of luxury.

Each summer my parents would rent a car and we'd drive the hour to my great aunt's house in Huntington, Long Island for a weeklong vacation. The big draw? A private, in-ground swimming pool and cabana house we could stay in.

The kids across the street would come over for a swim, we called the next-door neighbors Uncle and Aunt, and we barbecued our meals. It all felt very warm and wholesome, and so unlike what I was used to.

I always spent the first night on Long Island lying awake, unable to sleep thanks to the deafening drone of crickets outside my window. The wailing of city sirens was like a lullaby, but the sounds of nature felt somehow intrusive.

Long Island was only 40 miles away from home, but it felt much farther.

Where my path led me

I ended up marrying my high school sweetheart, a fellow multi-generation New Yorker, and we felt confident we'd stay in the city forever, like our fathers before us, raising our future kids on the same streets we loved so fiercely.

But life takes funny turns, and we wound up in Israel for a few years, and then landed in Long Island when my husband got a job at a hospital there.

We moved when our son was one month old, and everyone said how much better it would be to raise a child in the suburbs. We were skeptical at best.

Our move to the suburbs didn't come with any of the amenities one might expect. Hospital housing provided us with a subsidized two-bedroom apartment, which is quite large by city standards, but requires a walk up a flight of stairs, and doesn’t come equipped with modern luxuries like a dishwasher or washing machine, which I had always equated with suburban life. But my husband can walk to work, a rarity where we live, so we're able to get by as a one-car household.

Getting settled

Having a child helped me acclimate to suburban life. In my son's early, sleepless days, I would strap him into the cozy carrier where I could be sure he'd doze off, and I’d take to the streets, determined to explore my new neighborhood by foot.

I discovered a lovely park and library within walking distance, where my son felt grass for the first time and we took Mommy and Me classes that introduced us to both baby sign language and other local parents.

I learned that there is a vibrant Portuguese community in my area, complete with enticing restaurants and bakeries that would feed my burgeoning pao de queijo (cheese puffs) addiction. I found a grocery store I could walk to, though it was a bit of a trek, and stubbornly timed how long it would take me to walk to the farther Korean market where I could find specialty items I was used to easily obtaining in the city.

Slowly I went farther afield, hopping in the car to check out the stunning Gold Coast mansions that are right out of “The Great Gatsby,” the preserves that were once home to Theodore Roosevelt, and the many well-tended public gardens.

Come our second summer on Long Island, my son was a walking, water-loving toddler who relished every second we were at the community pool or nearby beaches. Never am I happier to live where we do than in the warmer months, when all manner of outdoor activity is at our fingertips. It's now our third summer here, and I've finally figured out how to easily obtain a pool pass, and which beaches I can access based on where I reside.

Home away from home

For all that I've grown to enjoy about living in the suburbs, though, I'm still a city girl at heart. We take the train into the city often, and my son gets a great thrill from taking the subway, seeing the crowded city streets, catching glimpses of taxis and buses and fire engines.

His grandparents all live in Manhattan, and we spend many weekends having slumber parties in cramped quarters, just to get a taste of all that our beloved city offers.

We have adapted to life in the 'burbs because that's what you do, and because there is so much to enjoy here. But my husband and I still have our hearts set on life in the city - if not this year, then in the next few.

I know that once we go back I'll miss the farms and beaches and big box stores, and I'll long for the well-stocked libraries and exciting museums. But we can always rent a car and make a vacation out of it.

After spending a lot of time in Italy, Ray and Terry Travaglione knew they wanted a Tuscan-style villa back home. So in 2002, they bought an idyllic piece of land on South Carolina’s Hilton Head Island and built one.

It’s not heavy the way some people think of Tuscan architecture, Ray said. “It’s not Gothic, but understated, with a Santa Barbara appeal to it. Every corner is rounded, as you would find in a Tuscan villa.”

There’s also a local flavor, with wood beams that were pulled from the Savannah River, he said. The home is on the market for $4.97 million with listing agents Dan Prud’homme and Tristan O'Grady of Carolina Realty Group.

Giant oak trees share the grounds with trees that recall Italy: lemon, lime, orange and fig.

Unlike central Italy, the property sits on the water, with a private beach alongside a deep-water dock. There’s also a lap pool that was designed on an angle, so swimmers can look up the Intracoastal Waterway.

The 6,671-square-foot home offers stunning water views, including from the chef’s kitchen, which boasts a 6-burner Viking gas stove, two dishwashers, a farmhouse sink and wood-beam ceilings. It features 4 bedrooms and 5 baths, a 1,200-bottle wine cellar and a guesthouse with a fully equipped gym.

The living and dining rooms boast a custom stone fireplace, cathedral ceilings and French doors that open to water views. Outside, there’s a 400-square-foot dock house with built-in seating and wiring for music and television.

The villa faces west across the waterway, which makes for breathtaking sunsets, Ray Travaglione said. “At the end of each day, there’s this little gift given to us by looking west.”

Selling this mansion in suburban Chicago ought to be a slam dunk for retired basketball star Scottie Pippen, who’s asking $3.1 million.

Selling this mansion in suburban Chicago ought to be a slam dunk for retired basketball star Scottie Pippen, who’s asking $3.1 million.