Carrying a mortgage is no small thing — it’s the largest debt many people will ever have — but it’s considerably harder when a home is valued below what’s left on the mortgage.

That situation is called “negative equity,” or being underwater, and many homeowners sank there in the wake of the recent housing crisis and recession. They are essentially stuck in their homes, unable in many cases to refinance or sell without taking a major financial hit.

At its most dire, 31.4 percent of U.S. mortgage holders were underwater. That was in the first quarter of 2012.

Three years later, the percentage is down by more than half, to 15.4 percent of U.S. mortgage holders, according to the first quarter Zillow Negative Equity Report.

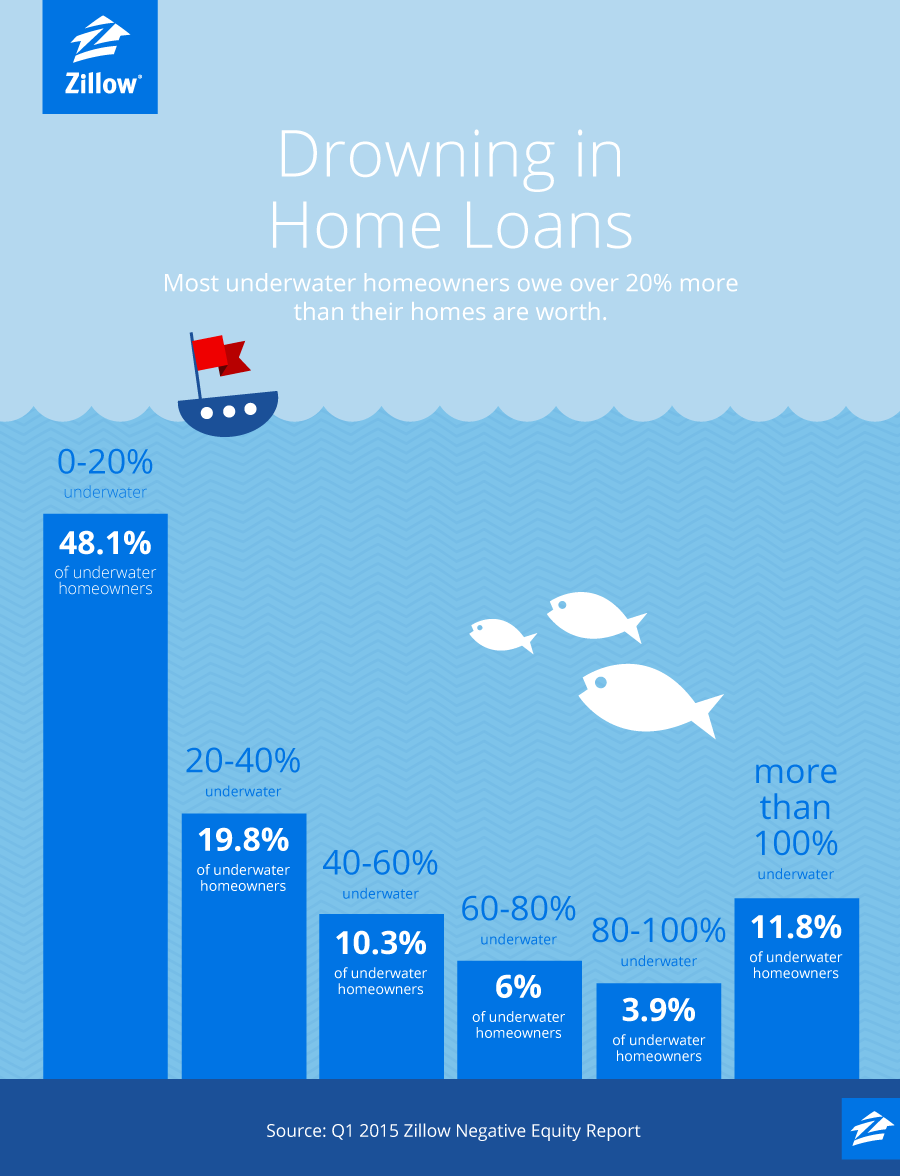

That’s 7.9 million homeowners, of which 11.8 percent — more than 930,000 borrowers — owe more than twice the value of their homes.

“It’s great news that the level of negative equity is falling, but what really worries me is the depth of negative equity. Millions of Americans are so far underwater, it’s likely they may not regain equity for up to a decade or more at these rates,” said Zillow Chief Economist Stan Humphries.

To compound matters, many borrowers — underwater and not — are nearing retirement, and some are facing increased mortgage payments, said Gerri Detweiler, director of consumer education for Credit.com.

Larger payments are looming for many people who participated in federal mortgage relief programs and for many who took out home equity lines of credit before the housing crisis.

“It’s not over for a lot of people. They can still be in a precarious situation if anything goes wrong financially,” she said.

In general, Detweiler counsels underwater borrowers to explore all their options before a financial setback forces them to make a decision they haven’t thought through.

Some people will find it makes sense to stay put until home values rise enough to pull them out of the financial hole, Detweiler said. Others won’t.

Renting out the property also will make sense for some borrowers, but the possibility of tax changes and unexpected expenses will make it less attractive to others.

Detweiler strongly recommends not walking away from a mortgage without getting legal advice.

“I find a lot of consumers don’t understand the implications of just giving up on their mortgage,” she said. In some cases, that can lead to unexpected taxes, garnishment of wages and seizure of bank accounts.

She also suggests that people see a housing counselor or bankruptcy attorney before they tap retirement savings, which can be spared in some bankruptcy proceedings.

For more information about mortgages and home values, visit Zillow Research or follow and ask questions of Zillow Chief Economist Stan Humphries on Twitter.

Here’s a question he fielded recently: Why do underwater borrowers keep paying? “In America, mortgage contracts are imbued with a moral context,” Humphries said.

Related:

- Even Inexpensive Homes Too Pricey for Many Workers

- Where Can Millennials Afford to Buy Homes?

- Zillow Ranks Best Markets for Buyers, Sellers

from Zillow Blog - Real Estate Market Stats, Celebrity Real Estate, and Zillow News http://feedproxy.google.com/~r/ZillowBlog/~3/AzAgvAncSKY/

via Reveeo

No comments:

Post a Comment